Ai-Media Technologies Ltd ($AIM.AX)

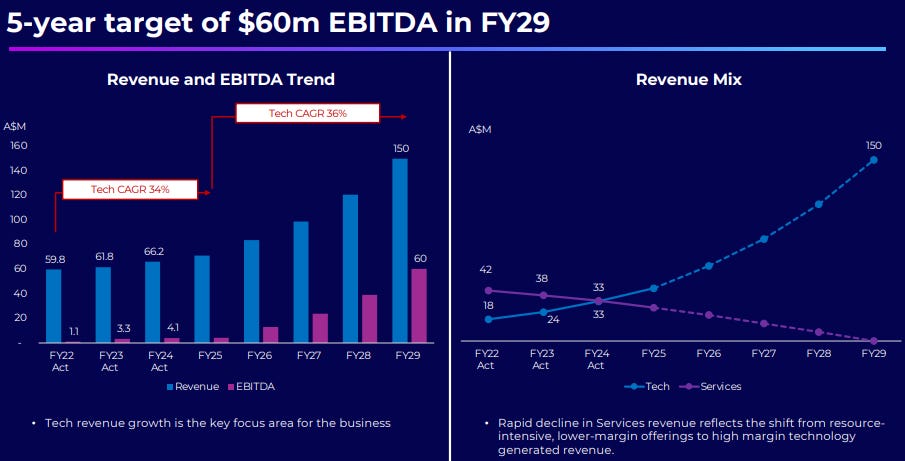

Don't be turned off by the name...Revenue is flat over a few years but the mix is moving from low margin legacy humans to scalable very high margin software/tech

$113m Mcap, $99m EV

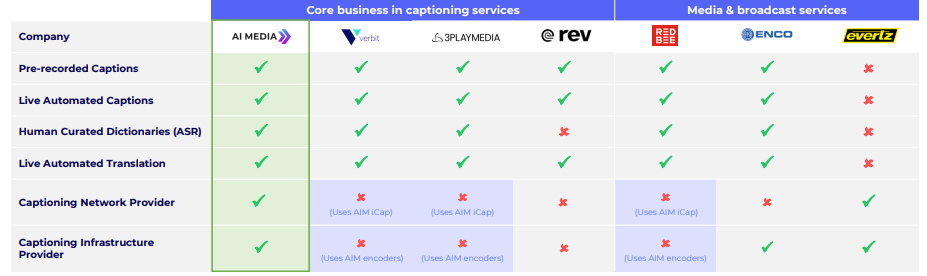

Ai-Media (AIM) provides captioning for live events & broadcasts. Everyone can do recorded video captions, the key here is Live. Through AIM’s industry standard hardware (encoders) & software (iCAP network) they have a competitive advantage & their competitors have to use both of these to provide Live captions. I believe AIM have ~80% market share of US live broadcast market in encoders & (a fast growing) 55% market share in iCAP network usage for captions (which I think is ~90% of US live broadcast captioning & is itself growing double digits).

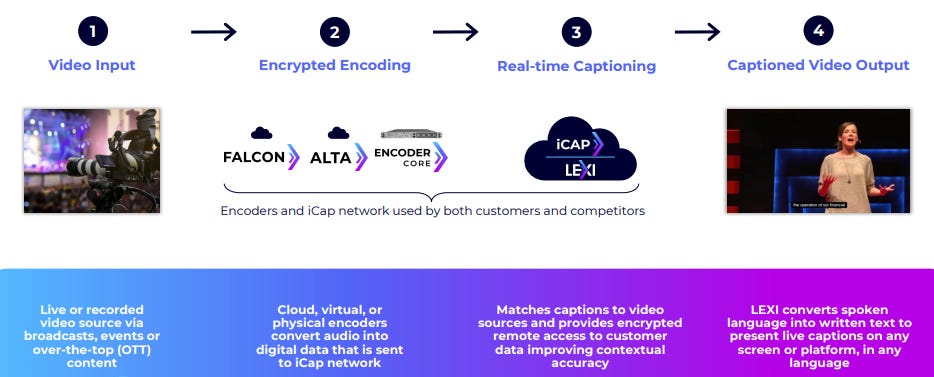

AIM’s Lexi Text (their live captioning product) uses big automatic speech recognition (ASR) engines (Speechmatics, Google, Microsoft etc) as an input to provide their product. So as these get better so does Lexi. Lexi surpassed human captioning accuracy 1H24.

The encoder takes the video stream in & isolates audio to highest quality, this data is then sent over iCAP network (AIM charge ~$2 per hour for competitors & there is no competitor network I believe) that connects encoders to everyone’s own AI models (or humans sitting at a computer) in the cloud. Then the captions go back across the iCAP network to the encoder & gets put back on the video synched up to speech.

I believe the big tech ASRs only comprise ~10% of the value in this chain, AIM gets the rest (eg. AIM charge ~$10 per hour and pay ASR $1 per hour.) Google is an AIM customer (see 18 August 2022 announcement).

I’m not going into a long description of the business, the more these notes become a burden the less (even less than now) that I will do. Read the 27 Nov 24 AGM address & presentation plus

’s note. I’m far from the first on this idea so calling out @lukewinchester9, @_max_wellth, @Driscoll_04 &AIM normally sell ~800-900 encoders p.a into the US (5 year replacement cycle). Currently there are 5865 encoders out there. AIM have recently moved into Europe & I think the results are already very exciting. They’ve sold 150 encoders fytd mentioned on 3 May 25. They sold 0 in FY22, 5 in FY23 and 55 in FY24.

Stock trades at 24x EV/EBITDA (4x EV/ARR (SaaS revenue only), 2.3x EV/Tech revenue (hardware + SaaS)). At 24x Ebitda (they expense everything) I might normally have a violent reaction but here you have a very high margin segment growing at >30% with a product that is better, faster and cheaper with a competitive advantage that keeps away competitors (encoders & iCAP). So you're providing a better product (higher accuracy captioning) at a significant cost saving (eg. Human costs ~$100 per hour vs Lexi ~$10 per hour) which not only wins market share but I think could open new opportunities for those who it was previously too cost prohibitive. Plus as it saves customers so much money they may decide to use it more which is great for AIM given the ~85% gross margins for SaaS and ~70% for the hardware (vs 44% for live human captioning). Plus the upside of any Lexi Voice (live voice to live voice in another language - $30USD per hour) if that proves attractive to live broadcasters.

I think the downside isn’t bad. They are FCF positive. Have $113m Mcap with $14m cash as at 31 Dec + $10.5 receivables vs $1.3 payables + any FCF from this 2H. And the easy wins in transitioning customers from human (own & competitors) to Lexi Text captioning should still occur.

Note the below is aspirational that the company has provided last result. Relies on products that are coming & other segment/geographical wins that they aren’t in yet. I don’t think the market is pricing in even a fraction of this & I am also not relying on it.

Other

1H25 Tech revenue grew by +1.2% - Look at deferred revenue balance growth, my understanding is AIM moved to upfront revenue model hence just a revenue recognition issue. Lexi iCAP network usage grew 48% YoY 1H25, so no slowdown.

B2B tech is hard to research so could something come along to replace encoders (AIM have software & hardware versions) & the iCAP network? Seems like answer is no as dominant in the US since the 1980s and would have to replace entire tech stack of live broadcasters but something to learn more about.

Previous chairwoman & substantial holder Deanna Weir has been selling which could be why stock is down from highs but I’m not sure. Some of the selling is for a Foundation so I wonder if its been done for non-financial reasons.

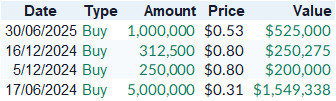

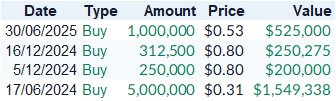

The CEO/founder Tony Abrahams owns 17.7% & has bought recently as below

Recent introduction of Long-Term Incentive Plan (8 May 25) - Only vesting condition is continued service. No financial targets is something I am unhappy with.

This is only a 1 pager, have obviously missed details and my grammar is bad but that’s not the purpose of a 1 pager. DYOR. This isn’t investment advice, I don’t know your circumstances. I obviously like the idea hence I hold a position in AIM at the moment, this could change. This is just to help me be clarify what I think. It’s based on my opinion of things that could happen in the future using publicly available information. Do your own research, I’ve probably made mistakes so do not rely on me. This ‘~’ means approximately or I guess.

Nice mate, thanks for the mention! Definitely think the chair selling and subsequent overhang is having an impact. Need a strong result or update to clear that I think...