Global Data Centres (ASX:GDC)

“Show me the incentive, and I'll show you the outcome.” - Charlie Munger

Simple & short (5 min read) investment idea with a catalyst driven by NEW significant alignment of incentives. It’s a heads I win, tails I don’t lose much idea.

The thesis is a narrowing of the current 48% discount to NAV with 2 key questions that need to be answered;

Key question number 1: Is the fair value NAV realistic?

Key question number 2: How/why will the NAV actually be realised?

COMPANY

Global Data Center Trust (GDC ) is an ASX listed real estate investment trust that specializes in the acquisition, development, and management of data centres

Market Cap is $121m, stock price is currently $1.57. Very illiquid.

Statutory NAV is $1.93, but importantly fair value NAV is $2.32 ($180m)

Fair Value NAV is made up of;

$112m - ETIX, a data centre operating business in France, Bangkok and Columbia. Portfolio of 10 operating data centres (5 wholly owned & 5 in JVs.) 6MW of capacity deployed with expansion potential up to 11.7MW.

$20.1m - Malaga, a data centre in Perth. 100% leased for 15 years to Fujitsu. Approx 2.5 years remaining on the lease plus 5 year extension option. Rent is $2.5m pa (CPI increases)

$37m - Airtrunk. Owns 1% of Airtrunk, an owner and operator of hyperscale customer data centres in Asia Pacific.

$10.7m Cash & other net assets

Key question number 1: Is the fair value NAV realistic?

ETIX - looks reasonable given the recent investment (Feb 23) by Eurazeo Infrastructure Partners (part of Eurazeo SE, a European listed, €4.9bn market cap, private equity and venture capital firm who manage €34.1bn)

Malaga - Based on rent of $2.5m p.a & 60% EBITDA margin (Small SME/Enterprise data centres usually about 80% margins in Australia, assuming 60% for Malaga given single customer concentration) gives $1.5m EBITDA. NXT (ASX listed data centre developer & operator) trades at 30x EBITDA (Trades at 3x book but to be fair a big portion of book is being developed.) Hence Malaga “trades on” $20.1/$1.5=13.4x EBITDA which seems ok given the short contract remaining and uncertain likelihood of renewal.

Airtrunk - Investment to date is $32.0m vs $37m value. Hard to gauge but given NXT value has held its stock price around $11-12 since July-20 (P/B has been around 3x since Feb-20.) seems ok.

So a significant gap to fair value NAV exists. A quick scan seems to show the fair value NAV assets is realistic. The Key Activists shareholders, who I think are great investors, would agree (I'm assuming.)

Key question number 2: How/Why will the NAV actually be realised?

Large activist shareholders on the register. Samuel Terry own 10%, Sandon Capital 5.6%

As per the 17th April announcement large activist shareholders have caused the investment managers of GDC (Lanrik Partners) to conduct a Strategic Review with an outcome of

"a pivot to a value realisation strategy. Under this strategy, GDC is unlikely to make new investments. Instead, Lanrik (investment manager) will seek to realise the value of GDC’s existing assets over the medium term through asset disposals"

Samuel Terry (GDC’s largest unitholder) has proposed changes to Lanrik’s remuneration model which is key to the realisation of value;

Base management fee changed from 1% to 0.5% of gross asset value. Additionally, Lanrik waive its right to termination and notice period fees.

Replacement incentive scheme - Performance Rights that vest upon "liquidity event" or 12mths after GDC's price reaches Relevant hurdle. The anticipated effect of adopting the Performance Rights Plan will be to more directly align Lanrik’s financial interest in GDC with that of its unitholders under the value realisation strategy. The hurdles will be adjusted for distributions and capital returns.

The waiving of termination and notice period fees is very important because the asset realisation strategy means liquidation of the company and hence Lanrik having nothing/little to manage anymore.

The Performance rights are key. Last half (1H FY23) the investment manager fees were $965,424, so $2m annually, but the proposed changes would halve management fees in favour of performance rights. Meaning the manager could earn $1m annually or say $8.6m in 12 months if the stock price got to fair value NAV ($2.3), and shareholders would be happy to pay this given a 50% increase in stock price.

While they may just want to remain as managers and asset gather they also have to be careful given the major activist holders would be unhappy with the big discount the shares have consistently traded at while Lanrik line their pockets, I assume this is what has led to this strategic review.

Value realisation is very likely within 36 months as "if the Tranche has not vested by the end of 3 years, the Initial Relevant Hurdles will increase at 10% p.a (including a catch-up clause from inception)."

RETURN/VALUATION

Therefore today you could;

Buy the entire company for $121m

Liquidate for $180m in Year 3

Pay $11.5m investment fees ($8.6m Performance Rights + $3m investment management fees)

Have $47.5m ($180m -$121m -$11.5m) of profit

This would be a 39% ROI or 12% CAGR over 3 years

I think the above scenario is actually below what is more likely because of 2 reasons;

It assumes liquidation at year 3 end. If you assumed 2 years then the return goes to 18%p.a as less time and management fees

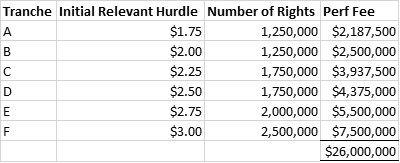

It assumes fair value NAV of $2.3. Samuel Terry's proposed changes to remuneration structure has relevant hurdle stock price from $1.75 to $3. Given the large premium listed data centre owners & operators trade at, fair value above the stated $2.3 is possibly something they believe given the proposed stock price range, and the manager would be incredibly incentivised, a $3 stock return would be massively lucrative for the investment manager $26m of performance right fees (~26 years of management fees under the new arrangement)

CONCLUSION

The investment manager Lanrik are massively incentivised to liquidate GDC assets at high values which the market is not currently assuming, and shareholders would be happy to see Lanrilk get paid very well given the big appreciation they would experience upon such an event.

While the market did initially react to the 17th April announcement of the pivot the a value realisation strategy, given the returns on offer, either the market is not believing of its success or the stock is to under the radar for most investors. I believe it's more under the radar given prior to the announcement this was a $92m market cap with 90 day average turnover ~$73k (excluding 17th March when Sandon & Samuel Terry bought in)

I am assuming the proposed changes to Lanrik’s remuneration are approved by unitholders in June 23 as who wouldn’t want the gap to fair value NAV to narrow?

Risks

The company doesn’t pay a dividend which means you earn no income while you wait for the value realisation.

The fair value NAV the company has put out could be wrong is obviously the biggest risk I think

This isn’t investment advice, I don’t know your circumstances. I obviously like the idea hence I hold a position in GDC at the moment, this could change. This is just to help me be clear about what I think. It’s based on my opinion of things that could happen in the future using publicly available information. Do your own research, I’ve probably made mistakes so do not rely on me.